Business model and investment policy

TRIG's Business Model

TRIG seeks to enhance the long-term sustainability of shareholder returns through:

- Portfolio diversification

- Responsible investment

- Value enhancement

To find out more about the interaction between these core elements, click the segments through to the business model page.

-

Responsible investment

-

Portfolio diversification

-

Value enhancement

Our Investment Policy

Our objectives

-

Responsible investment

-

Portfolio diversification

-

Value enhancement

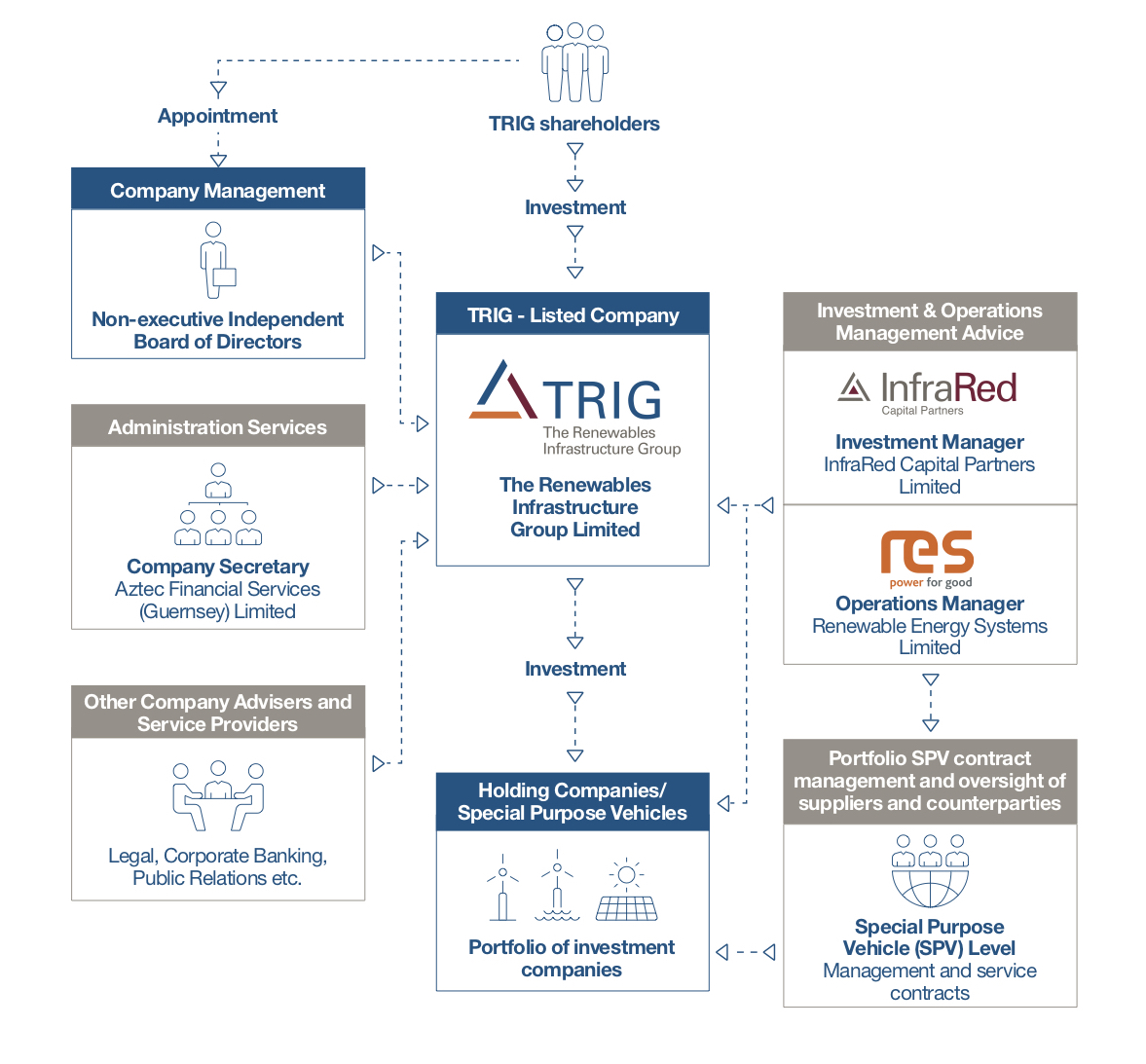

TRIG is an investment company whose shares are listed on the London Stock Exchange. As at 31 December 2024, TRIG had a market capitalisation of £2.1bn and owned a portfolio of renewable energy infrastructure projects in the UK, Northern Ireland, France, Germany, Spain and Sweden. TRIG’s group structure, including management structure and key service providers, is illustrated below:

The Company is a self-managed Alternative Investment Fund under the European Union’s Alternative Investment Fund Managers Directive. The Company has a board of independent non-executive directors whose role is to manage the governance of the Company in the interests of shareholders and other stakeholders. In particular, the Board approves and monitors adherence to the Investment Policy, determines risk appetite of the Group, sets Group policies and monitors the performance of the Investment Manager, the Operations Manager and other key service providers. The board meets a minimum of four times per year for regular Board meetings and there are a number of ad hoc meetings dependent upon business requirement. In addition, the Board has four committees covering Audit, Nominations, Remuneration and Management Engagement.

The Board takes advice from the Investment Manager, InfraRed, as well as from the Operations Manager, RES, on matters concerning the market, the portfolio and new investment opportunities. Day-to-day management of the Group’s portfolio is delegated to the Investment Manager and the Operations Manager, with investment decisions within agreed parameters delegated to an Investment Committee constituted by senior members of the Investment Manager.

Other key service providers to the TRIG Group include Aztec Financial Services (Guernsey) Limited providing Company Secretarial and Administrative services, Investec Bank PLC and BNP Paribas as joint brokers, Maitland/AMO as financial public relations advisers, Carey Olsen as legal advisers as to Guernsey law, Norton Rose Fulbright LLP as legal advisers as to English law, Link Asset Services (Guernsey) Limited as registrars and Deloitte LLP as auditor. Lenders to the Group’s revolving credit facility are National Australia Bank, Royal Bank of Scotland International, ING, Sumitomo Mitsui Banking Corporation, Barclays, Lloyds, BNP Paribas, ABN Amro, Skandinaviska Enskilda Banken (SEB) and Intesa SanPaolo.

The Board reviews the performance of all key service providers on an annual basis.

FAQs

- What are the features of the renewables market opportunity?

- How does TRIG set its business strategy?

- What are TRIG's investment risks?

- How does TRIG make new investments?

- How does TRIG construct its portfolio?

- What are TRIG’s key investment requirements and investment limits?

- What is TRIG’s approach to gearing?

- How does TRIG invest in renewable energy?

- How does TRIG invest in the energy transition?

- What are TRIG’s return targets?